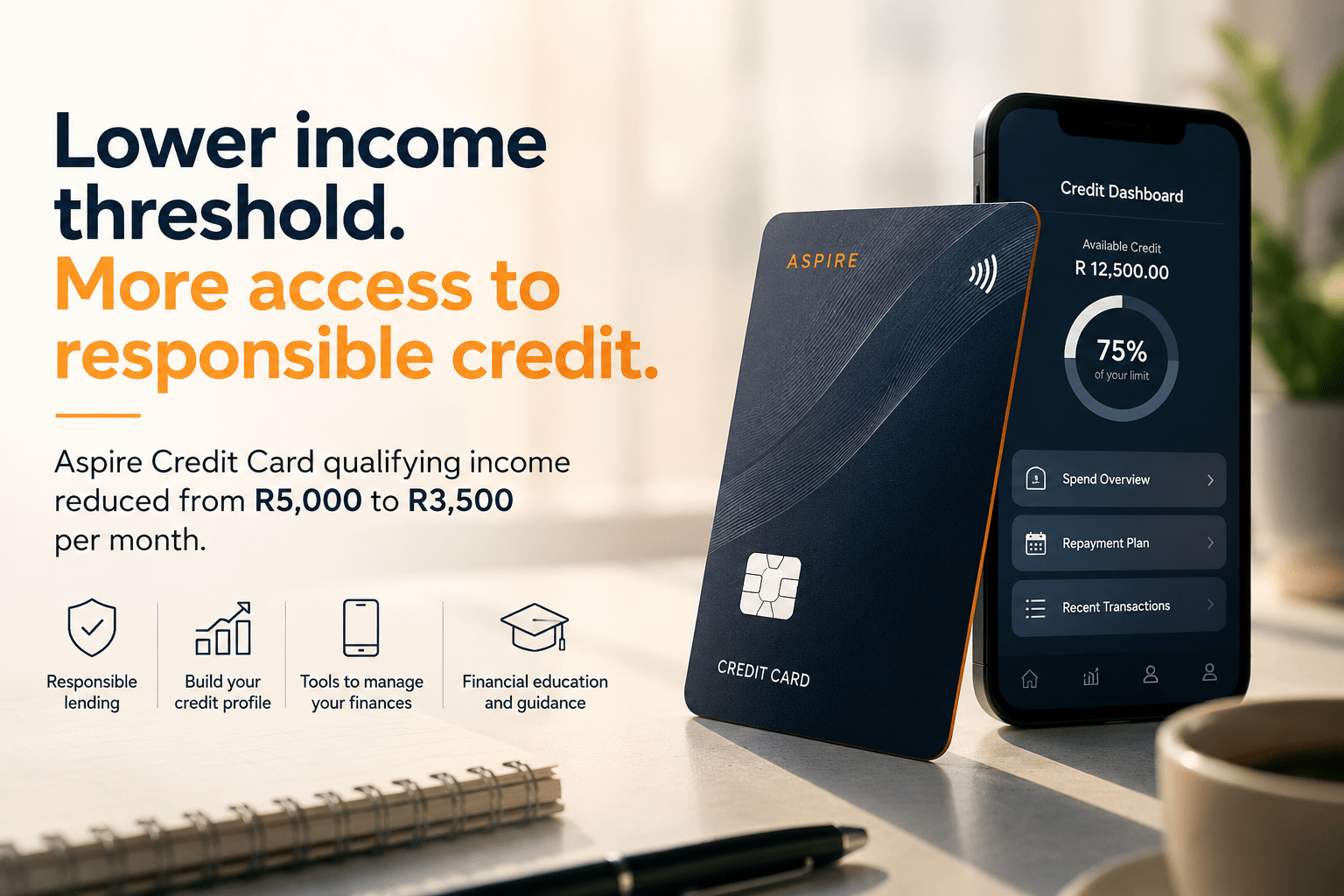

As South Africans continue to navigate rising living costs, access to responsible and regulated credit has become increasingly important. Recognising this need, First National Bank (FNB) has announced a significant change to its Aspire Credit Card offering by lowering the minimum qualifying monthly income from R5,000 to R3,500.

Effective from 7 July 2026, the adjustment is designed to broaden access to formal credit for qualifying customers while maintaining strict affordability and creditworthiness assessments in line with the National Credit Act.

Rather than expanding credit indiscriminately, FNB says the move is focused on helping more South Africans access structured financial products that support long-term financial wellbeing.

Making Formal Credit More Accessible

The revised income threshold forms part of FNB’s broader financial inclusion strategy, aimed at customers who are entering the credit market for the first time, have limited credit histories or are working to rebuild their credit profiles after previous financial challenges.

The bank says formal credit can play an important role in helping customers establish a positive financial record, provided it is used responsibly.

“Access to formal credit can help build a financial profile, but responsible lending is about far more than approving applications. This is not about giving credit access to everyone,” said Thabiso Tshabalala, Credit Card Product Head at FNB.

“It’s about ensuring customers enter credit in a way that is structured, transparent and supported with the information and tools they need to understand not only the benefits of credit, but also its costs and responsibilities.”

Responsible Lending Remains the Priority

FNB has emphasised that every Aspire Credit Card application will continue to undergo statutory affordability and credit assessments.

Reducing the qualifying income threshold does not guarantee approval. Instead, the bank says it allows more eligible customers to apply for a regulated credit product while ensuring lending remains responsible.

According to FNB, responsible borrowing begins with understanding how credit works, how repayments affect a customer’s credit profile and how consistent financial behaviour today can unlock future opportunities.

Tools Designed to Support Better Financial Decisions

The Aspire Credit Card includes several features intended to help customers manage credit responsibly.

These include:

- Clear repayment visibility.

- In-app tools that help customers monitor spending and available credit.

- Flexible repayment options.

- Structured credit limits based on individual affordability.

- Ongoing financial education and practical guidance.

The bank says these tools are designed to give customers greater confidence and transparency when managing their finances.

Understanding the True Cost of Credit

FNB is also encouraging customers to familiarise themselves with all costs associated with borrowing before making use of any credit facility.

The bank notes that certain transactions, including cash withdrawals and cash advances, may begin attracting interest immediately. Interest and applicable fees may also apply if outstanding balances are not settled within the applicable interest-free period.

Customers who consistently pay only the minimum amount due may ultimately pay more over time, while missed or late repayments can negatively affect their credit profile.

Understanding these obligations, FNB says, is an essential part of responsible borrowing.

Building a Stronger Financial Future

For many South Africans, establishing a healthy credit record is an important milestone that can improve access to future financial products such as vehicle finance, home loans and other forms of credit.

FNB believes responsible credit should support long-term financial goals rather than provide a short-term solution to financial pressure.

“Credit should never be used as a quick fix for financial pressure,” Tshabalala emphasised.

“Used responsibly, it supports future financial goals. Our role is to make that journey clearer, safer and more transparent.”

The bank also highlights that formal, regulated credit offers consumers greater transparency and protection than informal borrowing channels, where costs and conditions may be unclear.

By lowering the Aspire Credit Card income threshold while maintaining responsible lending standards, FNB aims to expand financial inclusion and help more qualifying South Africans make informed financial decisions that contribute to long-term financial progress.

{kind=link}